The Road to Financial Repression #2 // THE PAPER TIGER

The Road to Financial Repression #2 // THE PAPER TIGER

Why china will have to devalue the Yuan

(10-12 min read)

“At the heart of capitalism is creative destruction”

Joseph A. Schumpeter

Key Takeaways:

· China’s high growth over the past decades was driven by high investment and saving rates but this trend is unlikely to continue as it is plagued with substantial capital misallocation (real estate bubble, water and power shortages, bad demographics).

· China’s economic development very much resembles Japan’s one during the 1950-1980 period (high investment rate, central planning, strong current account surpluses) and could lead to the same phenomenon of “Lost Decades” (a combination of deflation and low growth).

· As the Chinese Communist Party struggles with the real estate and banking crisis, it will have to choose between devaluation or recession. Given the current internal context and the strategic importance of FX reserves in China, we believe devaluation is inevitable.

· Such devaluation will likely be met by tariffs on Chinese exports. Besides, the fall of marginal return on capital in China and the physical constraint on production indicate that higher prices (inflation) are poised to last.

PART I: THE IRON LAW OF ECONOMIC GROWTH.

1) The recipe of economic growth.

2) An illustration of capital misallocation: China’s water problem.

PART II: THE SIMILARITIES BETWEEN LATE 80’s JAPAN & PRESENT CHINA.

PART III: A DUAL SYSTEM & THE CONSEQUENCES OF A MANAGED EXCHANGE RATE FOR DOMESTIC MONETARY POLICY

PART IV: WHY CHINA CANNOT DEPLETE ITS RESERVES TO MAINTAIN THE PEG & WHY IT WILL EVENTUALLY DEVALUE

Introduction

Western investors have often succumbed to Orient’s charms. In the 80s, they believed Japan had invented a superior form of capitalism and was poised to become the world’s leading economic power. In the 90s, they hailed Asian values for the rapid growth of Southeast Asia and bet that the economic miracle would last forever[1]. This time, their love has fallen upon China. Once again, many westerners praise a “superior economic model” and expect China to become the XXIst century’s economic engine.

The pattern is clear: western analysts and market participants witness sustained growth in some distant region and then come up with cultural arguments to explain such success. In such matters, “culture” seems to be akin to the epsilon we use in physics to balance equations: what the observer fails to explain is necessarily due to cultural differences. Every time we hear about the “Chinese economic miracle”, it is about how efficient, laborious, and productive the Chinese people are and how prescient and smart their bureaucratic elites must be. Very rarely is it pointed out that China’s centrally planned development produces huge imbalances that can only stifle future growth, or that such development is built on a foundation of over-indebtedness, as was the case with Japan and Southeast Asia. Once again, everyone saw the tiger and almost everyone missed the paper.

In this month’s newsletter, we want to debunk the Chinese miracle and explain the extent to which it is built on an unsustainable pyramid of debt. Furthermore, we will explain why China’s debt problem is becoming ever more relevant considering the current real estate and banking crisis and why we think Chinese authorities might have to devalue the Yuan over the coming quarters/years. To articulate our point, we will first have to explain the dynamics of capital allocation in a bureaucratically managed system such as Communist China. Then we will focus on the specificities of the Chinese currency system and explain why we think the Chinese Communist Party (CCP) will most likely not deplete its huge FX reserves to defend the currency. Lastly, we will provide a way to exploit this asymmetric bet and draw the implications of this forecast being right for the global macro landscape.

PART I: THE IRON LAW OF ECONOMIC GROWTH

1) The recipe of economic growth

Economic growth is always and everywhere the result of a subtle combination of factors of production. As with any recipe, the proportions matter a great deal. When a factor of production is either overused or underused, it leads to suboptimal growth.

In the early 80s, China closed the page of communism and embraced a market-driven form of economic organization with Deng Xiaoping’s “Great Leap Forward”. At the time, China benefited from a large workforce, positive demographics and a vast territory filled with natural resources. Yet, China lacked capital. By welcoming foreign investors and offering attractive business conditions, China obtained the missing ingredient to its economic growth recipe.

Back then, the Middle Empire was an immaculate canvas waiting to be painted. There was very few roads, airports and factories, no subways, outdated housing, underdeveloped ports, and most of the population lacked basic education. Capital was so underused that any investment offered huge positive returns. Therefore, with the help of capital imports and a high savings rate, China fueled a massive and sustained investment boom that resulted in an era of high growth.

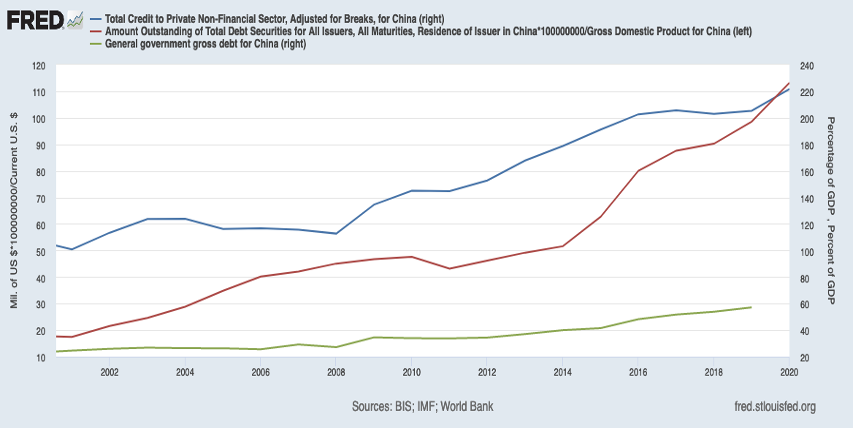

At some point in the 2000s, marginal return of capital started to fall (as is always the case). Yet, China was to a large extent a centrally planned economy, so it prevented any adjustment in its structure of production and tried to maintain its growth trajectory with debt and mortar.

What was then underused, started to become overused. As a result, debt grew faster than GDP (see below).

For the Chinese Communist Party, it was, and still is, very important to guarantee a certain level of GDP growth and employment. In practice, Beijing fixes GDP growth targets, which are constantly met by local administrators, as failing to do so is not really an option.

Such a development model is very effective, but also very inefficient since it prevents any capital reallocation. In a “normal” free market economy malinvestments are revealed by the arithmetic of profits and losses and rooted out through bankruptcies. When such losses occur, it stalls, or even reverts growth for a time, but as new entrepreneurs take control of depreciated capital goods and reallocate them to more productive uses, marginal returns on investment rebounds and growth eventually resumes.

By making GDP an input in the economic system, China has consistently impeded this Schumpeterian process. When a Chinese company fails, losses are not written off, because otherwise GDP targets could not be met. Similarly, when there is no profitable way to invest capital, local administrators still engage in economic activity for the sake of it. Consequently, the level of malinvestment (and overinvestment) in China is arguably one of the most elevated in economic history.

2) An illustration of capital misallocation: China’s water problem

The “fatal conceit” of Chinese elites and western panda huggers has been to consider that price manipulations have no consequences on capital allocation. In our opinion, there is no better illustration of the ills of price fixing than what some analysts have labelled “China’s water problem”.

As Gopal Reddy, the founder of Ready for Climate, mentions in this piece, China is home to 20% of the world’s population but it only possesses 7% of global freshwater resources. In other terms, the most important commodity on earth, is a scarce resource in China. On top of this water scarcity problem, China also has a water distribution problem: the 12 northern provinces account for 60% of agricultural land, 40% of the population, but only 20% of freshwater resources[2]. Therefore, people in this region live well below the threshold of water scarcity (defined by the U.N. as 1,000 m3 per person per year) and below the level of “acute scarcity” (500 m3 per person per year). At one point in 2012, the available supply of freshwater in Beijing, capital of the country and home to some 23 million people, was as low as 120 m3 per person.

The Chinese Communist Party has been aware of this issue for at least 17 years[3] but has not been very vocal about it as it lacks long-term solutions. As Charles Parton puts it in his in-depth piece China’s Looming Water Crisis, “China can print money, but cannot print water”.

For the moment, the Chinese people and the economy rely on aquifers (underground water) and the CCP imposes restriction during period of important hydric stress. Yet, as aquifers take thousands of years to replenish and are drying out very rapidly, this is totally unsustainable. The CCP also launched a grand project aiming at diverting water from the south to the north (South North Water Transfer Project), but it is yet too small to significantly alter the situation and will only be completed in decades.

Putting aside the implication for day-to-day life in China, this water scarcity issue poses an enormous constraint on industrial development. Many industrial processes require huge quantities of water (e.g. chip manufacturing or textile), but also demand a lot of energy, whose production is itself very water intensive. The main sources of power in China are hydro, coal and nuclear, which are all very dependent on water. Needless to say, that China cannot fill such water need by imports.

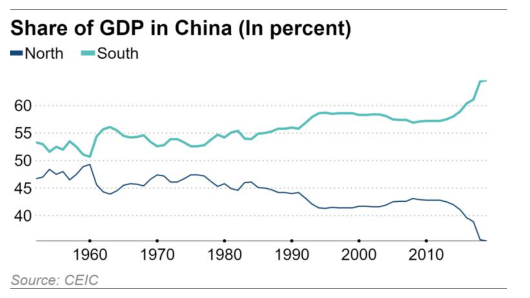

In a free-market economy, such scarcity would be priced in, so that entrepreneurs would be incentivized to save water. However, in China, the price of water is fixed by the government at an “affordable level”. Consequently, many capital allocators have been blind to this issue and have deployed their production facilities in areas where water is in very short supply, and/or resorted to production methods that are heavily water-intensive (e.g. Chinese farmers). The decline of GDP growth in North China and the recent rationalization of power that forced some manufacturers to temporarily shut-down their facility indicate that such constraints are already affecting industrial production at scale[4].

Besides revealing the economic imbalances caused by central planning, China’s water problem also confirms the trend toward higher prices and the likeliness of further monetary expansion in China. As China is the world’s workshop, halting of production due to power and/or water shortage will put an upward pressure on manufactured product’s prices, not only in China but in the whole world. Additionally, hydric stress will drive industry relocation within China, and it will likely force the People’s Bank of China (PBOC) to run an expansionary monetary policy in order to meet these new CAPEX needs.

Conclusion

To summarize, such an economic management model feels good on paper as GDP grows with each unit of spending. But it also plants the seeds for a gigantic economic downturn. When the adjustment eventually occurs, it either translates into “Lost Decades”, as was the case with Japan at the end of the 80s, or into a total collapse, as was the case with the USSR.

Let’s stress the fact that the adjustment is not an option; it can be postponed but can’t be avoided. A falling marginal return on investment combined with the political will to sustain GDP growth at all costs necessarily make the debt grow faster than GDP, which is totally unsustainable. At some point, the country reaches a debt ceiling, i.e. growth becomes insufficient to service the debt, or runs into physical constraints such as water scarcity, and the whole house of cards collapses.

The way in which the slump manifests essentially depends on the financial relationship between the domestic economy and the rest of the world. When the boom is financed by foreign money, it is often the reversion of capital flows that pins the bubble. Conversely, when the bubble has been inflated through the domestic financial system, it is the slowing pace of credit creation that makes the bubble collapse under its own weight. The Asian debt crisis of the late 90s falls in the first category, while the Japanese crisis at the end of the 80s belong to the latter.

The “Chinese economic miracle” of the past 30 years has a lot of similarities with the Japanese case. Yet, some clear differences remain as the financial and monetary systems of the two countries are very different in nature. In the next part, we will explore Japan’s experience and assess what it could tell us about China’s future. Then we will explain the extent to which differences in financial constraints could produce different outcomes.

PART II: THE SIMILARITIES BETWEEN LATE 80’s JAPAN & PRESENT CHINA

“Those who forget history are condemned to repeat it”

George Santayana

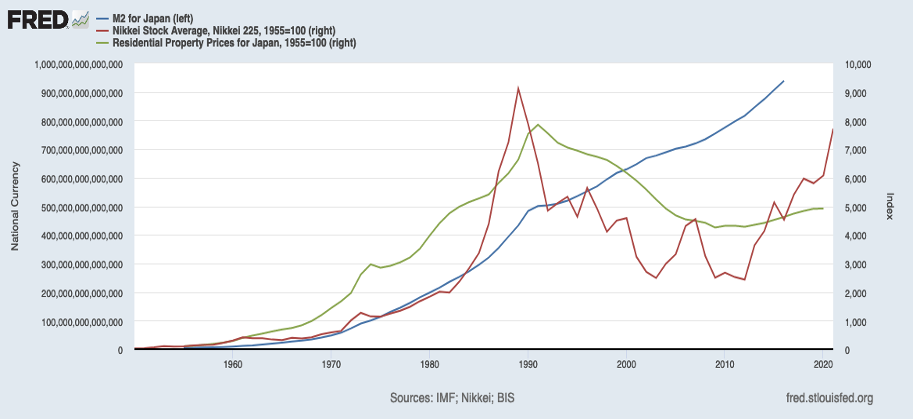

From the 60s to the 80s the Bank of Japan conducted a policy of lending quotas called window guidance[5]. The Bank of Japan gave lending targets to commercial banks, thus putting them in a position in which they had to lend even if there were no productive projects to lend to. As a result, Japan’s money supply expanded at a sustained pace for decades, causing one of the biggest real estate and stock market bubbles in modern financial history (see below).

At some point, Japanese households had 65% of their net worth in domestic real estate and the area surrounding the Imperial Palace in Tokyo was worth more than the entire state of California. In a “classical developed economy”, such as the U.S., real estate usually represents between 30 and 40% of households’ wealth.

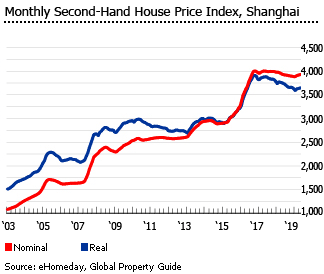

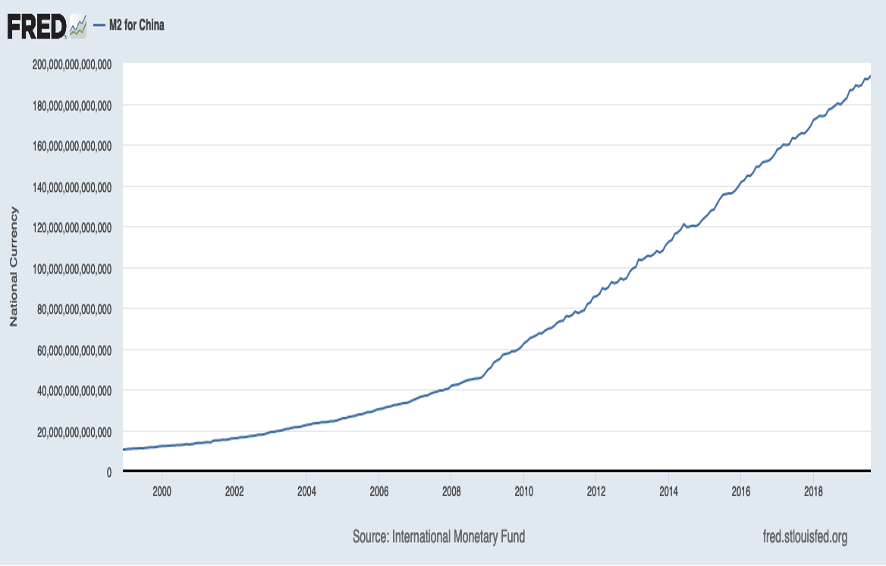

In China, banks also have lending quotas (because of GDP targets) and real estate currently accounts for 80% of households’ wealth (the latter can also be explained by the fact that Chinese residents have limited access to other financial assets -more on that later). As with Japan, such monetary policy has produced an explosion in M2 money supply and a real estate bubble in Tier 1 cities (see below).

In China, the share of the real estate sector is 2 or 3 times what it is in similar economies. In the U.S., real estate accounts for ~18% of GDP, approximately half of what it is in China. Therefore, the current real estate and banking crisis puts Beijing in a very tight spot: if they let the system deleverage, most of households’ wealth will be wiped out at a time when the CCP strongly signals its intend to shift from an export-driven to a consumption-driven economy, but if they bail out real estate developers and banks, they will produce undesired consequences such as reinforcing the wealth gap, downplaying moral hazard in a financial system already plagued by it and devaluing their currency (more on that later).

After the Japanese bubble burst, the Yen trended lower for more than a decade and growth was almost nil as Japanese entities were slowly deleveraging. Since Japan was a huge exporting nation, the devaluation increased exporters’ competitiveness, thus allowing the country of the rising sun to maintain important trade surpluses. Those surpluses acted as a sort of valve: they protected foreign demand for the Japanese currency and thus prevented an even dire downturn. Yet, this slow deleveraging process translated into sluggish growth for decades with second order effects such as terrible demographics (low growth, high asset prices and high debt-levels often discourage people from starting families).

Again, this is very similar to the current Chinese situation. China has terrible demographics, partly due to the one-child policy and partly because young men don’t have the financial means to buy a house and start a family. The average piece of property in Chinese cities costs around 30 years of median income, while it stands between 6 and 12 in the West. Furthermore, like Japan, China is a big exporting nation and can thus count on its trade surplus to act as a “valve”, and in this regard, we could expect China to go through the same “lost decades episode”.

However, the parallel ends here. Indeed, contrary to Japan, China has a managed exchange rate and a semi-closed capital account (capital controls), altering the dynamics at play.

PART III: A DUAL SYSTEM & THE CONSEQUENCES OF A MANAGED EXCHANGE RATE FOR DOMESTIC MONETARY POLICY

“A nation’s exchange rate is the single most important price in its economy; it will influence the entire range of individual prices, imports and exports, and even the level of economic activity”

Paul Volcker

China has an on-shore and an off-shore financial system. The first one is RMB denominated, very insulated, and totally controlled by CCP bureaucrats who can restructure liabilities at will. The second one serves as an interface between China and global capital markets. The former is a closed circuit, and the latter is a two-way street allowing foreigners to invest capital in China and Chinese corporations to raise capital from abroad. The bridge between the two is the CNY (Chinese Yuan), China’s external currency. The People’s Bank of China (PBOC) uses its FX reserves to maintain the CNY at par with the CEFTS basket (see below).

This dual system is very important to consider in the context of the current downturn as it puts a constraint on the Chinese domestic monetary policy.

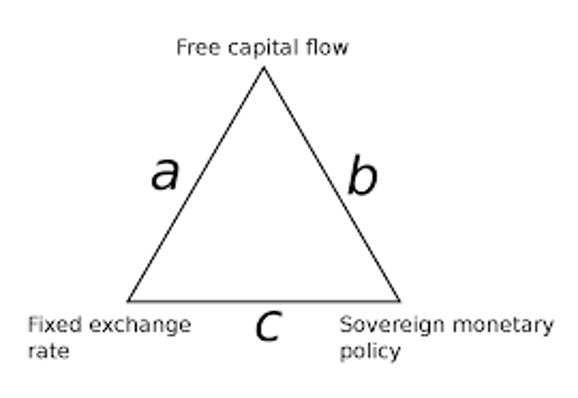

This all comes down to what economists refer to as “the impossible trinity” (see below) which states that a sovereign country cannot simultaneously have free capital flows, a managed exchange rate and an independent monetary policy. An economy could only have 2 out of 3, i.e. is on one of the sides of the triangle. So, by pegging their currency to a basket of foreign currencies, Chinese authorities have relinquished their monetary independence. Basically, this is because interest rate differentials between the anchor currencies and the pegged currency would cause divergence in supply and demand dynamics such that the peg could only be maintained by spending FX reserves to close spreads.

If, for example, Chinese monetary policy was looser than that of the U.S., one could borrow CNY and buy U.S. treasuries with no, or little, FX exposure and still have a positive carry (i.e. a free lunch). The consecutive capital flights from China would weaken the CNY and hence force the PBOC to spend its FX reserves to thwart the devaluation.

In this example, we assume that capital can freely flow in and out of China, which is not really the case in practice: if you are a foreigner, you can invest in and out of China, but as a Chinese national you can’t. Through their oversight on the domestic banking system and by closing alternative financial channels, such as Hong-Kong or Bitcoin, the CCP does everything in its power to keep capital ashore. Nevertheless, as over a long enough period, people always find ways to circumvent capital controls, we can still place China on the “a” side of our triangle (free capital flows + fixed exchange rate).

Furthermore, while China’s capital account is semi-closed, there are ways for financial institutions to raise capital in foreign currencies through unregulated channels, such as the shadow banking system. So, although the PBOC could lower its interest rate without too many adverse consequences in the short run, it would be a tremendously dangerous thing to do over an extended period because financial institutions, big corporations and some individuals could take advantage of the situation.

So, the logical thing to do for the CCP would be to lower rates to alleviate the cost of servicing the humongous amounts of debt present on Chinese entities’ balance sheets. Yet, as the U.S. is on a trajectory to raise rates, this could force a devaluation of the CNY, or a slow bleed of FX reserves. As China has the highest level of FX reserves in the world (3.2Tn$ at least), many think the CNY peg is unbreakable. We, however, think that China doesn’t have the luxury to ease and maintain the peg. Let’s explain why.

PART IV: WHY CHINA CANNOT DEPLETE ITS RESERVES TO MAINTAIN THE PEG & WHY IT WILL EVENTUALLY DEVALUE

"Self-reliance is the best defense against the pressures of the moment."

Carl von Clausewitz.

We already alluded to the idea that the CCP cannot let the crisis unfold without doing something about it, but now is the moment to expand our argument.

As the Chinese financial system is already plagued by moral hazard, Beijing is likely to let some investors, real estate developers and bankers fail before intervening, especially since some bankruptcies could help purge excesses from the system. A total absence of intervention, however, would surely cause an unmitigated economic disaster with very important political ramifications for the leaders in place. This is due to the viral nature of a debt-deflation crisis in a fractional reserve system. If insolvencies cascades are not eventually backstopped, asset prices fall, unemployment rises, cash-flows rapidly deteriorate, so do investment and consumption levels, all in a vicious loop that can last many years (~30 years in the case of Japan). As the authority of the CCP relies heavily on an implicit contract with the population about the growth of GDP, employment levels, wealth and living standard, there is little chance that Xi Jinping would sit idly by while the economy sinks.

Another reason supporting the scenario of an intervention is the proportion of household wealth tied to the real estate market. Although a small decline in real estate prices could prove beneficial to Chinese social structure by lowering the cost of owning a home, a large one would surely create an inverse wealth effect and discourage people to spend, which would worsen the crisis. Besides, we should recognize that although China is not a democracy, it functions with similar political incentives as western democracies: Chinese politicians cannot be voted out of office, but they still need popularity to cement their authority, so they would rather kick the can further down the road.

So, assuming that the CCP will have to intervene at some point, it raises the question of “how”.

There are basically two possibilities:

· easing monetary policy and letting the CNY devalue,

· or easing monetary policy while at the same time using reserves to maintain the managed exchange rate at current levels.

We have 3 reasons to think the latter is unlikely:

1) FX reserves are not just a financial asset but rather a geopolitical asset for China.

2) There are a lot of precedents for this, and it always ends up with a devaluation.

3) Lowering rates while maintaining the peg would give huge incentives for private entities to borrow in foreign currency and could hence add an external debt problem on top of the internal one.

The first argument in favor of the devaluation is the maintaining of their financial “weapons of mass destruction”. As the reader surely knows, China’s position as the world manufacturer allowed them to run large trade surpluses with the rest of the world and, therefore, to build huge FX reserves. Those reserves are more than just financial assets. They are a geopolitical weapon.

If the U.S, and/or their allies, start to be overly confrontational, China can threaten to cause a financial meltdown in western markets by dumping its Treasuries and other USD-denominated securities all at once. It may not seem like it, but it is way more efficient a threat than is deploying aircraft carriers in the Pacific Ocean. China’s FX reserves are its best geopolitical asset, so we do not believe for a second that they will squander their war chest just to avoid a devaluation, especially at a time of elevated geopolitical tensions.

The second argument is a political one and can be stated that way: it is not because a country has the means to maintain its peg that it will chose to do so during a crisis.

In 1997-98, when capital exited Southeast Asia en masse every peg broke (with the notable exceptions of HK and Singapore). For some countries, such as Malaysia, Thailand, or the Philippines, it was inevitable as they lacked the reserves to defend their currency. For others, such as South Korea or Taiwan, it was a political choice. Since they had some of the largest FX reserves in the world, they arguably had the means to defend their peg, but they choose not to.

Why did Taiwan, who had the 3rd highest level of FX reserves in the world, devalue? Simply because of the impossible trinity! By maintaining the peg, they would have to raise rates during an economic downturn, which is politically untenable since it is equivalent to shielding savers’ wealth at the expense of everybody else’s welfare. We believe the same to be true for China, especially given the size of the real estate sector, households exposure to it and the skewed distribution of savings in favor of the wealthy and the government. Furthermore, it is rather dubious to expect the second largest economy in the world to tolerate having its monetary policy dictated by foreigners.

Third, and lastly, even if we imagine that the PBOC lowers rates and maintains the CNY at current levels, we would then be in a situation in which anyone could borrow RMB and use an unregulated channel to invest in higher-yielding US-denominated securities. In practice this would be difficult for most entities, but the very nature of credit creation in China and the opacity of the private credit system invites us to think that it could well be done in huge amounts even if only by a small cohort.

In conclusion, while devaluation seems unlikely at first sight, it appears that in the long run it would be the only working medicine. We think that a 10 to 30% devaluation would suffice to avoid a messy financial restructuring and an ensuing crisis, but also that the CCP will likely wait until it has no other choice. So, there is little chance of this happening over Q1 2022, especially with the Winter Olympics taking place in China.

To be clear, although we have a high level of confidence in our analysis, the reader must understand that this is quite a bold forecast and that there is a high likelihood of us being wrong. Nevertheless, we consider this to be a very asymmetric bet: as the CNY is tightly managed, implied volatility is very low, so out-of-the-money options on CNY/USD are quite cheap even for long duration. Unfortunately, there are very few instruments allowing retail investors to easily get such exposure (there are 2 ETFs, SCNY in London and XBJF in Germany, that are short CNY and long USD, but to our regret, we haven’t been able to find derivatives on those).

Now, let’s conclude and rapidly discuss the implications of this forecast for our main thesis of financial repression.

Conclusion

There is no denying that China witnessed an impressive and rapid economic development and is now one of the leading economic powers on this planet. However, many financial, intellectual, and political elites in the West also overpraise China’s model and overestimate its real strength, mostly because they see the tiger and miss the paper (debts).

Interestingly, this is nothing new under the sun. In the 80s, we were told that the USSR, and then Japan, would surpass the U.S. as the world leading economy. Those prophets were wrong then and are wrong again because they extrapolate growth trajectories without ever questioning their sustainability.

The USSR, Japan, and now China, achieved impressive growth by sustained overinvestment. As they all fought the process of capital reallocation, they all suffered from drastic capital misallocations, which some have called “bridges to nowhere”[6].

At the core of the beliefs in those economic miracles lies the very simple mistake of equating GDP in a Schumpeterian economy with GDP in a centrally planned economy. In the former, GDP is an output, a measure, albeit imperfect, of the economic growth in productivity, a measure of the systems’ efficiency. In the latter, GDP is an input of the economic system, a target to be met by printing enough money. This makes a huge difference because in the second case, GDP says nothing about the effectiveness with which production factors are mobilized. It can be productive, or it can just be blind and wasteful economic activity. We just can’t know since, sadly, centrally planned systems don’t take consumers preferences as gauges for the meaningfulness of economic activity.

There is a case to be made about the fact that the specific and unconventional structure of China’s financial system renders the illusion even more lasting and convincing. Chinese shadows come to mind.

To the outside world, China’s economy seems healthy because the mess it created within its border is not reflected in the outward-facing system. The only thing that supports this mirage is the enormous FX war chest China uses to interface with the dollarized global economy. Although such system is difficult to grasp initially, when it is understood, it is more predictable than our free-floating currency system with free-capital movement because the volatility that is suppressed somewhere will necessarily surface somewhere else. China won’t escape the laws of financial gravity. It can only suspend their effect for some time and then experience the fall all at once.

We don’t mean that China will experience an USSR-style collapse anytime soon, but rather that it will have to make tough choices to avoid such a catastrophe. Presently, this means dealing with a nasty crisis that is the result of 15+ years of exponential debt build-up, and in the face of it, a moderate devaluation seems to be a small price to pay.

Lastly, we want to point out that China is the manufacturer of the world and hence that in the eventuality of a devaluation, western countries would react promptly by imposing tariffs (among other sanctions). The reaction would vary from country to country. The U.S. would likely move swiftly, while Europe would show some initial restrain. So, while such a devaluation would be deflationary at first, we think it will then turn inflationary, not least because it would surely accelerate the trend toward industry re-onshoring. Such an inflationary forecast is even reinforced by the perspective of production inefficiencies caused by water shortages (and the related power shortages), which are ever more frequent in China.

In our first newsletter we explained that inflation is here to stay and that governments are likely to exploit it to deleverage the system by caping real yields at negative levels. Most analysts believe inflation will be transitory partly because they expect a continuation of the deflationary forces coming out of China. For all the reasons laid out here, we could well see a sustained trend toward higher prices.

This is the second edition of a monthly Newsletter dedicated to macroanalysis for the 2020 decade. Following Newsletters will be available on substack (link here) and will delve in more depth into this core thesis of Financial Repression. Many other investment opportunities, pertaining or not, to Bitcoin will be discussed in coming editions.

We would like to thank Michael Pettis, Kyle Bass, Gopal Reddy, Charles Parton, and Richard Werner as the thesis hereupon laid out owes much to the fine work of those gentlemen.

Disclaimer

This Newsletter should not be considered as financial advice. Its content is for educational purposes only. Readers should do their own research.

We are doing our best to prepare the content of this site. However, Institut Bitcoin cannot warranty the expressions and suggestions of the contents, as well as its accuracy. In addition, to the extent permitted by the law, Institut Bitcoin shall not be responsible for any losses and/or damages due to the usage of the information on our website.

By using our website or downloading this newsletter, you hereby consent to our disclaimer and agree to its terms.

The links contained on our website may lead to external sites, which are provided for convenience only. Any information or statements that appeared in these sites are not sponsored, endorsed, or otherwise approved by Institut Bitcoin. For these external sites, Institut Bitcoin cannot be held liable for the availability of, or the content located on or through it. Plus, any losses or damages occurred from using these contents or the internet generally.

[1] The Asian Debt Crisis, Birth of the Age of Debt, Russell Napier

[2] Charlie Parton, “China’s Looming Water Crisis” China Dialogue, 2018, https://cdn.chinadialogue.net/content/uploads/2020/05/20093454/China_s_looming_water_crisis_v.2__1_.pdf

[3] Rob Schmitz, “A warning for parched China: a city runs out of water”, Marketplace, 2016, https://www.marketplace.org/2016/04/25/warning-parched-china-city-runs-out-water/

[4] https://www.reuters.com/technology/many-apple-tesla-suppliers-halt-production-china-amid-power-pinch-2021-09-27/

[5] Richard Werner, Princes of the Yen: Japan’s Central Bankers and the Transformation of the Economy, Routledge, New edition (25 avril 2003)

[6] https://carnegieendowment.org/chinafinancialmarkets/75355, Michael Pettis